Why Out-Featuring Revolut Is the Wrong Goal

Imagine a 30-person fintech a year into its Series A. The board deck says "super app." The roadmap reads like Revolut's feature list from two years ago: cards, FX, vaults, stocks, crypto, maybe travel insurance — every line item owned by the same engineering org. Six months in, the team would notice that shipping the seventh feature takes three times longer than shipping the second. Every new module would touch the same auth flow, the same ledger, the same KYC pipeline. By month nine, the founder might find themselves hiring quarterly to outrun a problem that hiring cannot fix: the codebase is a stack of features pretending to be a platform.

Most founders I talk to in 2026 are facing this exact fork — and they're framing it wrong. The question isn't "how do we ship features as fast as Revolut?" The question is "what kind of company do we have to be so that we don't need to?"

KEY TAKEAWAYS

The competitive moat in super apps is platform shape, not feature count. Revolut-class incumbents win by absorbing new modules at constant cost; vertical super apps see per-module cost rise with each release.

Two architectural paths exist, and they diverge irreversibly around module #3. The vertical-monolith path optimizes for time-to-first-feature; the modular-platform path optimizes for time-to-tenth.

Horizontal services — auth, ledger, identity, compliance — are the load-bearing decisions. Modules can be rewritten; horizontals cannot, not without a re-platforming year.

Most "build vs buy" debates in super-app teams are mis-scoped. The right unit of decision is the module, not the company; differentiated modules get built, boring modules get integrated.

The Hidden Problem: You're Competing With a Runtime, Not a Feature Set

The instinct, once your first card product is live, is to build the next feature. Then the next. The hidden problem is that the third, fourth, and fifth features each cost more than the previous one — not less — because they all share infrastructure that wasn't designed to be shared.

Gartner's analyst coverage of the super-app category names the architectural shape directly:

"Super apps are built as platforms to deliver modular mini-apps that users can activate for personalised app experiences."

Jason Wong, VP Analyst at Gartner, via Integrated Finance

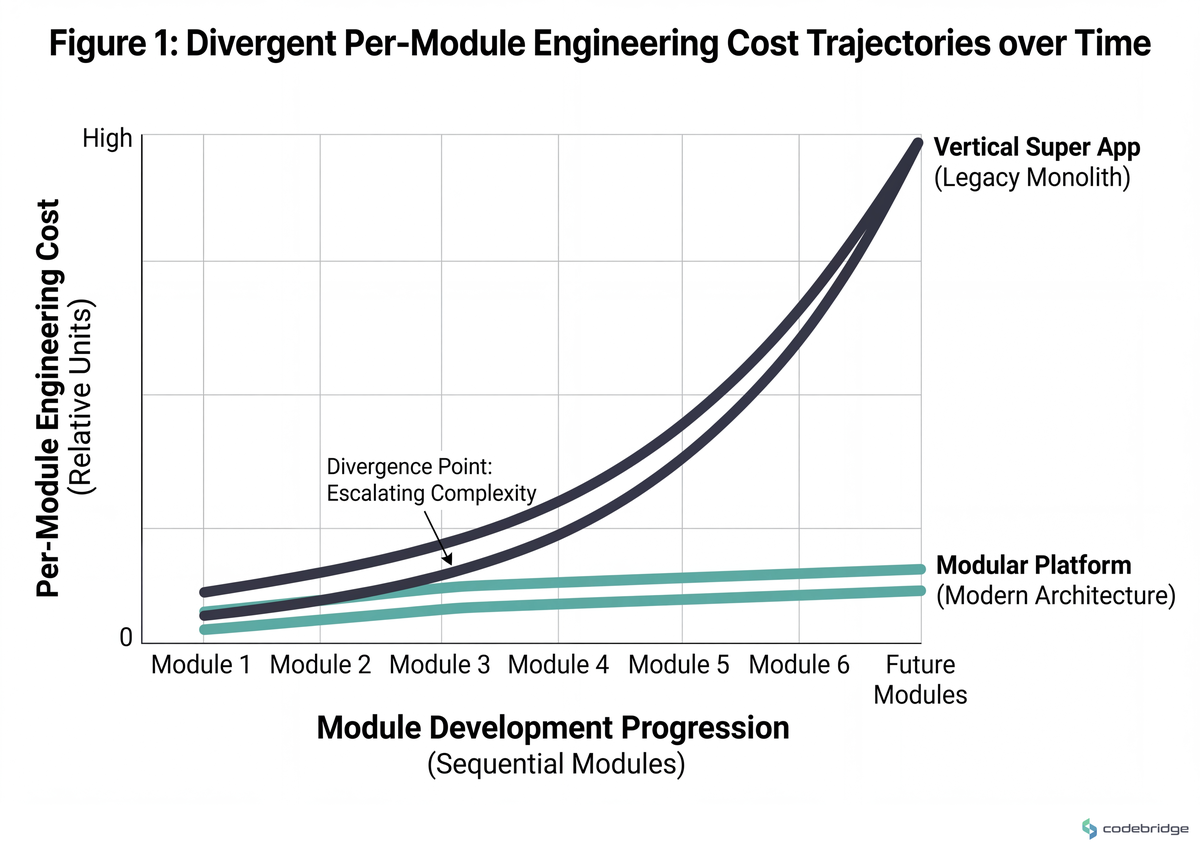

The word that does the work in that sentence is platform. Revolut-class incumbents organize their architecture as horizontal services that mini-apps consume, not as a feature stack. When they add stocks, crypto, or business banking, they're not extending a monolith; they're registering a new module against an existing runtime. That's why the marginal feature ships at marginal cost. The comparison below shows where the two paths diverge:

If your shape is wrong, you can hire faster than your competitor and still lose. The board will be pleased with the headcount chart and confused by the velocity curve.

Two Stories From the Field

We worked with a ~25-person LatAm neobank on a six-month engagement to plan their second-year roadmap. The before-state: their card product, FX, and a savings module were each shipped by a separate squad, but every squad was modifying the same authentication service and the same ledger schema. New features required all-hands integration weeks. The after-state, ~four months post-replatforming: a horizontal identity service, a single double-entry ledger with module-scoped accounts, and a documented contract that any new module must call rather than extend. The unlock was not technological cleverness — it was a governance decision: no module owns the auth or ledger code path. Lead time for a new module's first vertical slice dropped from roughly a quarter to roughly a sprint.

Now imagine the inverse: a mid-size European fintech that would try to add lending in year two without that horizontal split. Lending requires its own KYC depth, its own credit-scoring callouts, its own dispute flow. Without horizontal services, the lending squad would end up forking the auth code "just for now." The auth service would become two services maintained by no one. By the next compliance update, both would need patching independently. The pattern this illustrates is that horizontal services aren't a "nice architecture" choice — they're a forcing function that prevents organizational drift.

The Pattern: Companies That Win Build the Runtime First

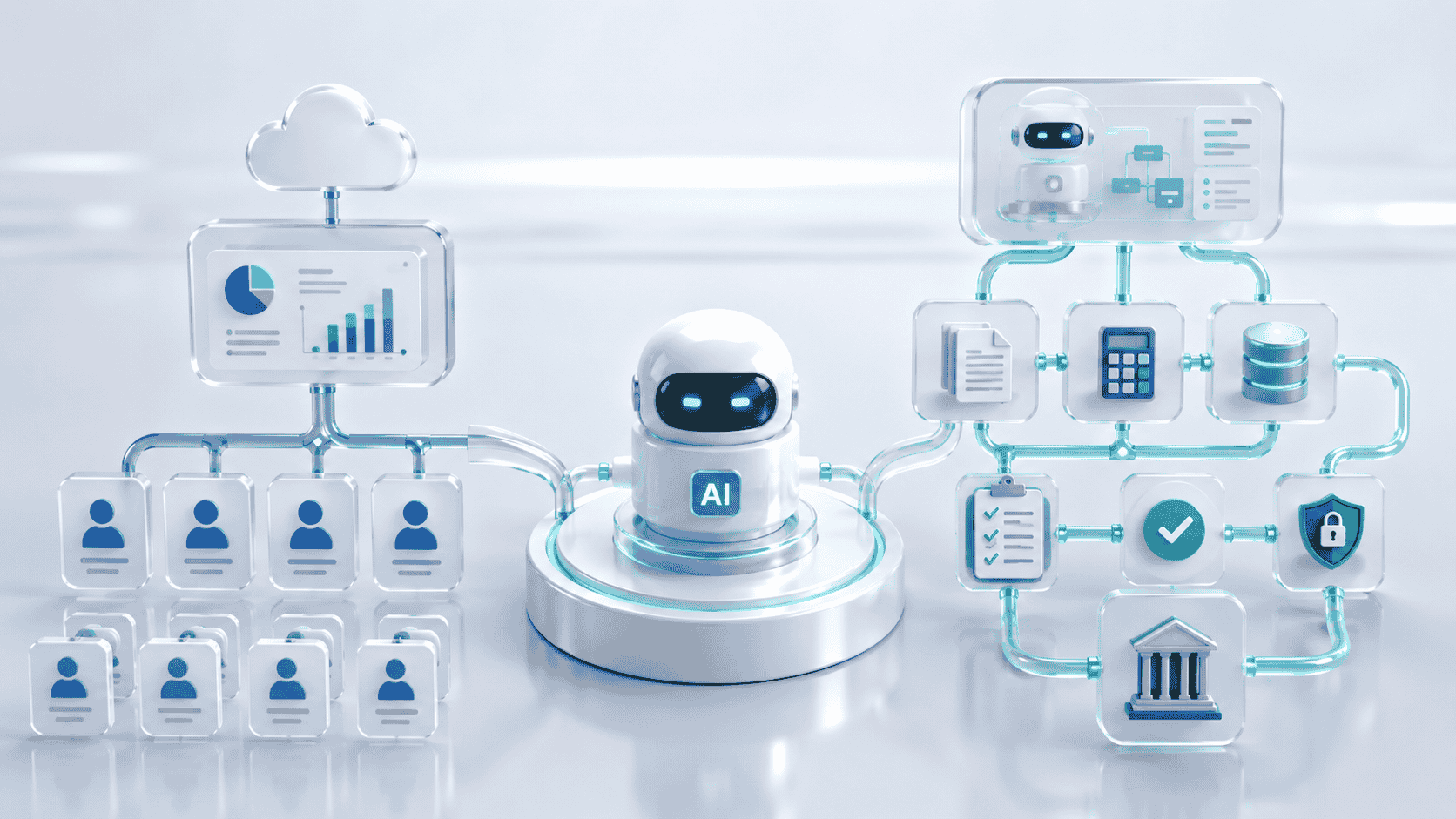

The teams that successfully compete in the modular super-app space made one decision early that the others didn't. They picked the runtime layer — the substrate that hosts modules — before they picked their second feature. Everything downstream is downstream of that decision.

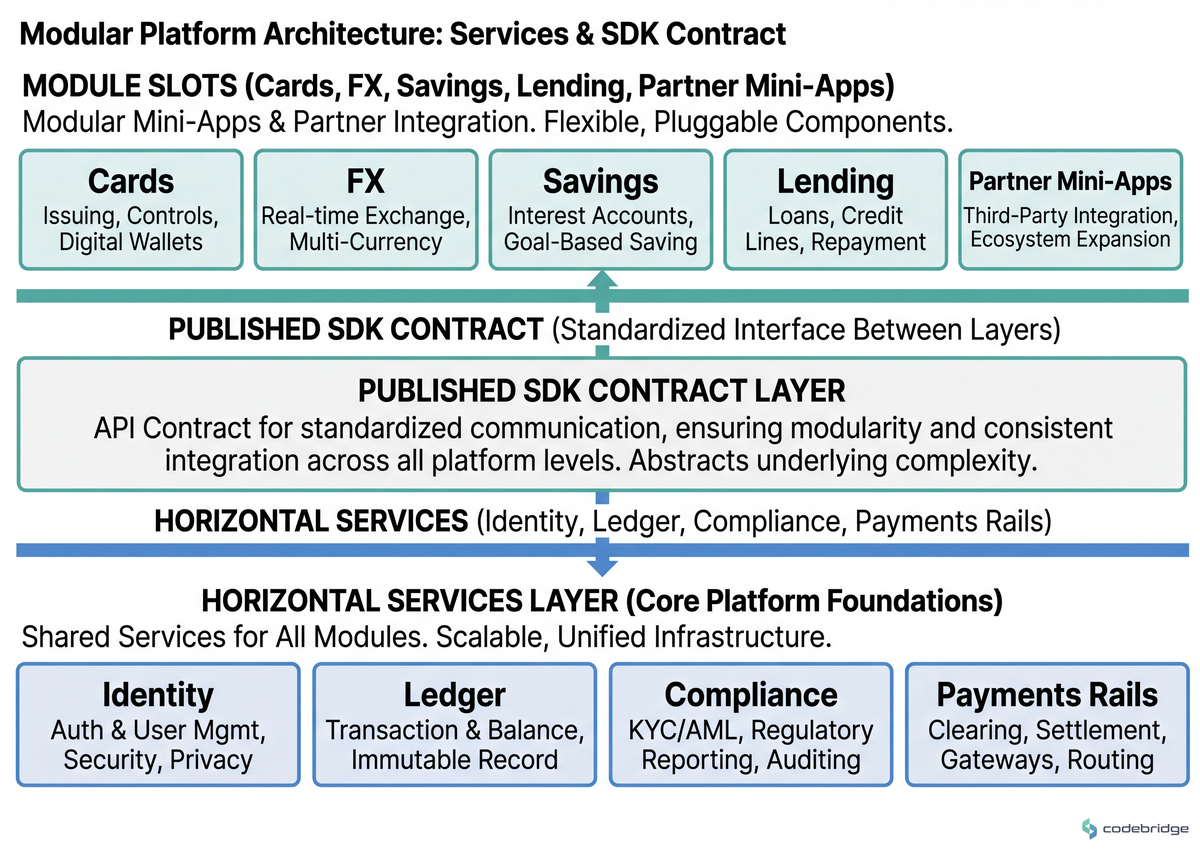

The architecture below shows what the runtime-first shape looks like:

The diagram captures something the comparison can't: modules are interchangeable, and partners can occupy module slots on the same terms as your internal teams. That's the single most important property a super app can have.

Framework: Four Decisions That Determine Whether You Have a Platform

1. Set your platform tax before module #3 ships

Decide the revenue or cost split between platform and modules before the platform is load-bearing for more than two features. Concrete threshold: if you have three or more revenue-generating modules without a documented internal accounting model, you are about to start a political fight that will be settled by whoever shouts loudest in the next exec meeting. The model should answer: who pays for the auth team's headcount? Module squads, the platform PnL, or central? Answer it on paper, then publish.

2. Pick the runtime layer before the second feature

The "runtime" is the contract every module calls into for identity, transactional state, money movement, and compliance attestation. A working signal: write down the API surface a partner-built mini-app would have to call. If you cannot draft that surface in a one-page document, you don't have a runtime — you have a tightly coupled feature set with module ambitions. Concrete pattern: an opaque, signed module token issued by your identity service that travels with every cross-module call; the module never sees user PII directly.

3. Govern the horizontal surfaces, not the modules

The four surfaces that must remain centrally owned: identity, ledger, compliance, payment rails. Every other surface is negotiable. Measurable signal: when you added your last feature, did the team modify code inside any of those four? If yes, you've started to fork your horizontals; budget a quarter to consolidate before adding the next module. The cost of consolidating now is roughly one squad-quarter; the cost of consolidating after module #6 is roughly one engineering org-year.

4. Build differentiated modules, integrate boring ones — with a written threshold

Suggested threshold: build in-house only when the module is (a) a primary acquisition driver, (b) directly differentiated from incumbents, or (c) generating >15% of activation. Otherwise, integrate a partner mini-app behind your runtime contract. The discipline matters more than the threshold itself — a written rule prevents the founder reflex of "we'll build it ourselves, it's only three sprints" applied serially to twelve modules over two years.

Verdict: Which Path Is Yours?

Return to the hypothetical 30-person fintech from the opening. If they completed the modular-platform shift, by year two their lending squad would not be forking auth — they would be calling it. New market launches would be configuration changes, not code releases. Hiring would lag rather than lead the roadmap. That's the demo case completed in the framework's terms; the synthetic-ness is the point. The decision the real version of that company faces is the one you face.

| Decision Criterion | Path A: Vertical Super App | Path B: Modular Platform |

|---|---|---|

| Time-to-first-feature | Faster (weeks) | Slower (1-2 quarters of platform work first) |

| Cost of feature #10 | ~3-5x cost of feature #2 | ~roughly the same as feature #2 |

| Partner mini-apps possible | No (or only via screen-scraping integrations) | Yes (first-class slot in the runtime) |

| Compliance update cost | Touches every module | One horizontal change |

| Best for | Single-product fintechs, narrow verticals, regulated niches with <5 planned modules | Founders who genuinely intend to compete at the super-app surface area |

Pick Path A if your honest five-year plan is fewer than five modules, your competitive surface is one or two regulated products done excellently, and your team is under 20 engineers. Path A wins on time-to-revenue and is a perfectly reasonable answer to "what kind of fintech are we?"

Pick Path B if your roadmap involves five or more modules, you intend to host any partner-built functionality, or you are explicitly positioning against a Revolut-class incumbent. The platform tax up front is real, and it is the price of admission to the category.

Pick neither if you cannot answer "what is our differentiated module?" in one sentence. Founders and CEOs in this position should not be choosing an architecture; they should be choosing a wedge product first.

The default for founders and CEOs of fintech super-app companies in 2026 is Path B — but only if they can credibly fund the first two quarters of platform work before the board demands more features. If they can't, Path A is honest. The dangerous answer is the third one: starting Path A and quietly hoping it becomes Path B without the platform investment. That's the path that produced the 30-person company in the opening.

The 30-minute artifact: draft the one-page API surface a hypothetical partner-built mini-app would call against your stack today. If you cannot complete it in 30 minutes, that is your most important roadmap signal this quarter.

Considering the platform shift?

Talk to Xi Labs about a runtime-readiness review of your current super-app architecture.

Diagnostic Checklist: Is Your Stack a Platform Yet?

Run these against your current system. Each maps to a specific failure mode that compounds with module count.

When you shipped your most recent feature, did the team modify code inside the auth, ledger, identity, or compliance service? Yes / No (Yes = forking your horizontals)

Could a partner team — given your SDK and a sandbox — ship a mini-app to your runtime without your platform engineers in the deploy path? Yes / No (No = no runtime exists)

When you onboarded your most recent regulatory market, did you ship a code release or a configuration change? Code / Config (Code = compliance is per-module)

Does each module own its own writes to the ledger, or do they all call a shared ledger service with module-scoped accounts? Own / Shared (Own = double-entry will eventually disagree across modules)

If your most senior platform engineer left tomorrow, how many in-flight module deploys would block on a single replacement? <2 / 2-5 / 5+ (5+ = you are one resignation from a quarter of slippage)

What percentage of your published 12-month roadmap could a competent partner build against your runtime, with no special access? <10% / 10-30% / >30% (<10% = you have a feature stack, not a platform)

Is your platform team's headcount funded by module squads, central PnL, or undefined? Module / Central / Undefined (Undefined = the political fight is coming)

Scoring: Count the "platform-side" answers (No, No, Config, Shared, <2, >30%, Module-or-Central). 6-7 = healthy modular foundation. 3-5 = at risk; budget a re-platforming quarter before module #5. 0-2 = you are operating a vertical super app with platform-scale ambitions. The math will not be kind.

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript